Advisory Shares : Complete Guide from Investors and Company perspective

You've likely come across this concept in numerous Shark Tank pitches, where founders offer advisory equity at a nominal value to sharks in exchange for their expertise and time to help with business growth and decision-making. Let's delve into the lifecycle of these advisory shares and explore their benefits and potential legal and tax implications.

Introduction:

Many individuals often confuse advisory shares with ESOPs and Sweat Equity shares issued under Sections 62 and 54 of the Companies Act 2013, respectively. However, it's crucial to emphasize that sweat equity, as per Section 54 of the Companies Act, can only be granted to employees, directors (including independent ones), or promoters. ESOPs are specifically intended for the company's employees. Hence, the concept of advisory shares is distinct from the aforementioned arrangements.

Advisory Equity is a straightforward option where a specific number of shares, usually equity, are allocated to advisors. These Shares are commonly allocated to consultants and advisors who offer consultancy services and advice to support the company's growth. This concept is popular among early-stage startups in India and worldwide.

These shares are generally allotted under the provisions of Section 42 read with Section 62 of Companies Act 2013

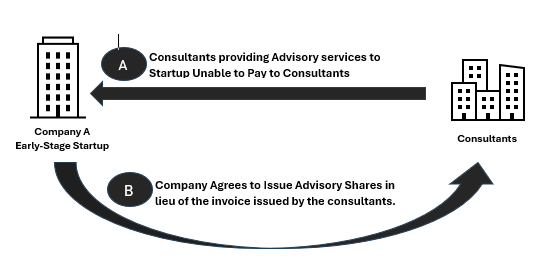

Early-stage startups, often facing liquidity challenges in paying consultants for their services, issue advisory shares in exchange for their consultancy fees.

Life Cycle of Issuing Advisory Shares:

Case 1:

Consultants raises an invoice to the company for, say, ₹5,00,000. Company A is having a Fair market value of shares of ₹ 1000 per share.

Therefore Company A will issue 500 Shares for the invoice amount to the consultants.

Case 2:

Consultants have started providing advisory services under the condition that the company will issue 200 equity shares at a nominal value of ₹10 each.

In this case consultants will pay ₹ 2,000 for the shares allotted to them to vest their options.

Taxation of Advisory Shares:

If advisory shares are issued below their Fair Market Value (FMV), the difference between the FMV and the consideration paid will be taxed in the hands of the investors receiving such shares. Later when the investors sell those shares capital gains will be attracted, based on the period of holding it will treated as Long-term or Short term Capital gains in the hands of investors and taxed at the applicable rate.

If shares are allotted to investors in lieu of their raised invoices, the company issuing advisory shares should deduct TDS under Section 194J of the Income Tax Act, 1961, at the applicable rate.

Individuals aren't subject to GST unless their annual income from all services exceeds INR 20 lakh. However, if advisory equity is allotted to a company instead of an individual, the company needs to pay GST at a rate of 18% on this amount.

Disclaimer: The content of this article is for information purpose only and does not constitute advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer to relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc. before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that the Author / Finncounts is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof.